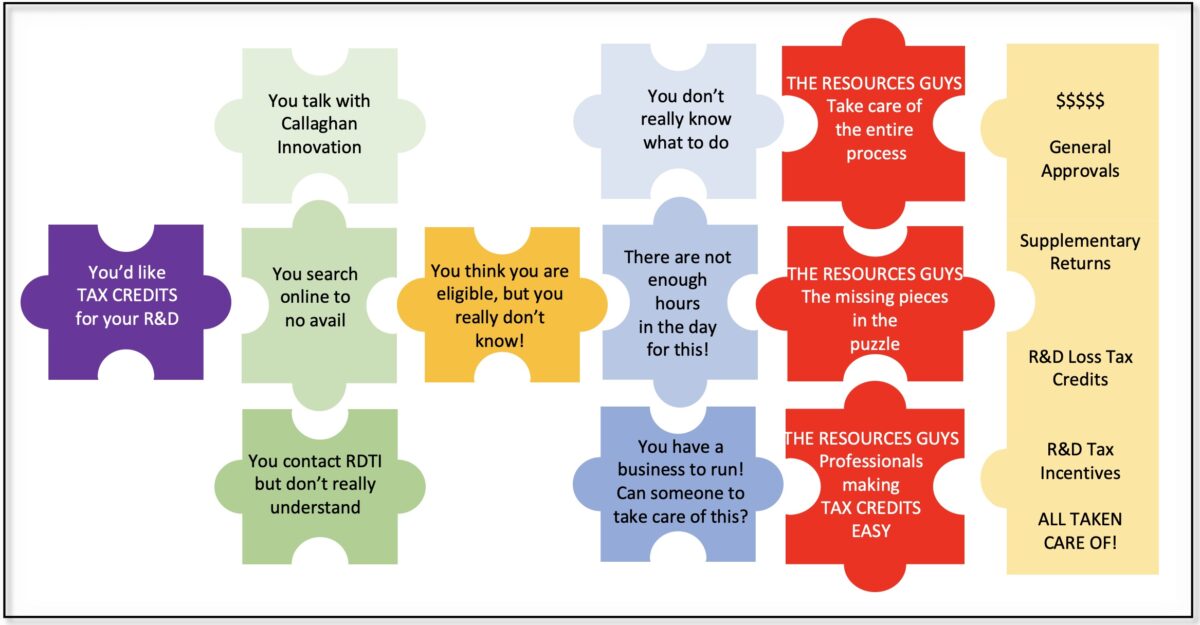

R&D Tax Credit (RDTI)

New Zealand’s R&D Tax Incentive (RDTI) gives eligible businesses a 15% tax credit on qualifying research and development expenses. This R&D tax credit supports innovation by helping companies recover part of their R&D spending and improve cashflow. To qualify, businesses must spend at least $50,000 annually on eligible R&D in New Zealand. An additional 10% of supporting activity costs can relate to overseas R&D activity. All R&D activities require General Approval, providing upfront certainty before businesses lodge their R&D tax credit claim. Approval can cover one to three income years.

R&D Loss Tax Credit

If your business is in a tax loss position, you may still claim New Zealand R&D tax credits. Businesses without sufficient income tax payable may qualify for refundable R&D loss tax credits, delivering effective cash back support. Refundable R&D credits are designed to help smaller and growing businesses facing cashflow challenges. This refundable R&D credit is calculated at 28%. When combined with the standard 15% R&D Tax Incentive, eligible businesses may access a total benefit of up to 43%.

R&D tax credits (RDTI)

In New Zealand, the R&D tax credits have replaced traditional government-funded R&D grants as the primary mechanism for supporting innovation. While both schemes aim to encourage investment in R&D, tax credits offer a broader, more sustainable framework for ongoing innovation.

At the resources guys, we help businesses navigate the R&D tax credit system with clarity and confidence. Whether you’re transitioning from legacy R&D grants or exploring R&D tax credits for the first time, our team provides practical, end-to-end support so that we can ensure your claim is accurate, compliant, and optimised for maximum value.

R&D tax credit expertise

Our expertise ensures your business captures the full value of R&D tax credits. As a result, we support every stage of the claim process – from identifying eligible activities and preparing technical documentation, to engaging with Inland Revenue when required.

If you’re seeking cash refunds for innovation or want certainty around your R&D claims, we’re here to make the process seamless, strategic, and effective.

Contact us to find out how the resources guys can help your business unlock greater value through the RDTI.

R&D loss tax credits (RDLTC)

If your business is not yet generating taxable income, you may still qualify for refundable R&D tax credits under the R&D loss tax credits (RDLTC) scheme. This enables eligible companies to receive a cash refund, providing vital funding to fuel ongoing innovation and product development.

For early-stage, loss-making R&D businesses, this can be a critical cashflow advantage. TRG can help you access this support with confidence, ensuring compliance and maximising the refund available.

Talk to us to learn how your company could benefit from RDLTC support in New Zealand.

Who we are

Founded in 2000, TRG – the resources guys – has earned recognition as one of New Zealand’s most trusted R&D tax consultants. Since then, we have specialised in helping innovative businesses access the R&D Tax Incentive (RDTI) and refundable R&D loss tax credits. Over the past two decades, our team has secured more than $100 million in R&D benefits for clients. As a result, we turn research and development investment into measurable financial advantage.

How we help

Our team combines technical expertise with practical commercial insight. In fact, we work across New Zealand’s diverse industries – from technology and software to manufacturing, agri-tech, and health. Whether you need full-service management of your R&D tax incentive claim or targeted support, we tailor our services to fit. In addition, we assist with General Approvals, Supplementary Returns, and audit defence, ensuring your business remains compliant.

Global partnerships

For complex and large-scale R&D programmes, we collaborate with Alvarez & Marsal, a leading international professional services firm. This partnership therefore strengthens our ability to manage sophisticated R&D tax credit claims. Furthermore, it ensures we align with global governance and compliance standards while supporting New Zealand businesses.

Get in touch

Contact TRG today to discover how our R&D tax consultants can support your innovation strategy. We help maximise returns through New Zealand’s R&D Tax Incentive and related programmes. As a result, your business can improve cashflow while gaining certainty and confidence in claiming R&D tax benefits.

LET’S TALK ABOUT YOUR R&D PLANS

LET’S TALK ABOUT YOUR R&D PLANS

R&D tax credit services

R&D Tax Incentive Claims Unlock the full value of your R&D through New Zealand’s R&D Tax Incentive. We guide you step-by-step: • Checking your eligibility • Preparing claims with the right technical detail • Submitting applications correctly • Maximising credits while staying compliant

General Approval Applications A strong General Approval gives you certainty and confidence in your R&D programme. We prepare robust applications that: • Clearly set out eligible Core and Supporting activities • Address MBIE’s requirements • Reduce the risk of disputes or rejection

Supplementary Returns Your Supplementary Return is where the detail counts. We provide expert support to ensure: • Technical descriptions meet compliance standards • Costs are properly coded and substantiated • Your claim is consistent and defensible

Audit Defence & Record Keeping Audits are part of the RDTI environment. We act as your safeguard by: • Reviewing and strengthening documentation • Establishing clear record-keeping systems • Representing and supporting you through IRD or MBIE queries

Key relationships

We work closely with MBIE’s R&D Tax Incentive (RDTI) specialists, who support Inland Revenue in assessing scientific and technological eligibility. Their role strengthens confidence in New Zealand’s innovation system by ensuring R&D claims are credible and well-supported.

learn more

We work closely with MBIE’s R&D Tax Incentive (RDTI) specialists, who support Inland Revenue in assessing scientific and technological eligibility. Their role strengthens confidence in New Zealand’s innovation system by ensuring R&D claims are credible and well-supported.

learn more

Inland Revenue administers the R&D Tax Incentive (RDTI) and Research & Development Loss Tax Credit (RDLTC). We work directly with their teams to ensure claims meet legislative requirements and withstand review. Their guidance helps businesses unlock cashflow advantages from eligible R&D expenditure.

As part of Alvarez & Marsal’s Global Tax team, we connect New Zealand innovators with international R&D expertise. A&M’s global reach and technical insight complement our local knowledge, giving businesses access to best-practice R&D tax credit strategies and compliance support worldwide.

The IRD maintains a register of Approved Research Providers (ARPs) for the R&D Tax Incentive. Engaging an ARP allows businesses to claim RDTI support without needing to meet the $50,000 minimum R&D expenditure threshold. Explore the current list of providers on IRD’s website.